History Rhymes: The Language Before the Break

Before the market breaks, the words change. Consumers adapt before they collapse. Investors sell labels before they read balance sheets. And the best capital waits for the moment when discomfort gets

Nobody wakes up and says, “The regime has changed.”

They say the grocery bill is stupid. The car payment feels heavier. The mortgage rate makes moving impossible. The CEO says the customer is selective. The Fed says it needs more data. The newspaper says uncertainty is elevated. The strategist says investors are waiting for clarity.

Then, months later, everyone pretends the shift was obvious.

It never is. Not when it matters.

Regime changes usually arrive as vocabulary problems. The first crack is rarely the index. It is the language around the index. Executives stop talking about growth and start talking about flexibility. Retailers stop talking about pricing power and start talking about promotions. Consumers stop talking about upgrades and start talking about waiting. Governments stop talking about frictionless trade and start talking about strategic capacity. Credit investors stop asking only about spread and start asking about maturity.

At first, none of this sounds dramatic. It sounds temporary. A cautious consumer. A volatile energy market. A few tariffs. A geopolitical flare-up. A refinancing issue. A supply-chain adjustment. A data-dependent central bank. A wall of worry.

Nobody says the model is broken yet. They just start using different words.

For most of the last thirty years, markets spoke the language of efficiency: run lean, outsource, scale globally, carry less inventory, own fewer hard assets, use cheap debt, buy back stock, trust supply chains, trust central banks, trust that inflation will stay contained, trust that refinancing will be available, trust that the grid, ports, labor pool, energy system, and geopolitical order will sit quietly in the background while the income statement gets optimized.

That language worked because the world rewarded it. Capital was cheap. Inflation stayed low for long stretches. Global trade lowered costs. China absorbed industrial complexity. Energy was treated as available. Supply chains were long but functional. Central banks had room to cut. The market paid for elegance.

Now the words are different. Tariffs are not just politics. Energy is not just a commodity chart. AI is not just software. Defense is not just a budget line. Debt is not just accounting. Supply chains are not procurement. Power demand is not a utility footnote. Consumer caution is not sentiment noise.

None of these words feels dramatic on its own. But together, they tell you the same thing: the old assumptions are getting more expensive.

The official data does not show collapse. The economy is still moving. People are still spending. Companies are still hiring. Deals are still getting done.

But more of it takes effort now. More of it depends on financing, timing, energy, inventory, and the consumer’s willingness to absorb one more increase.

The point is not that everything is breaking. The point is that more things now require a second look. The old market paid for efficiency. The new market is learning the price of insurance.

Not insurance as a product. Insurance as a condition of survival: cash, inventory, spare capacity, domestic production, multiple suppliers, low leverage, control of critical inputs, access to power, time before maturity, and the ability to keep operating when the cheapest assumption stops working.

This has happened before. Not as a clean rerun.

The point is not to force today into one old period. The point is to notice which parts of the old periods are showing up again.

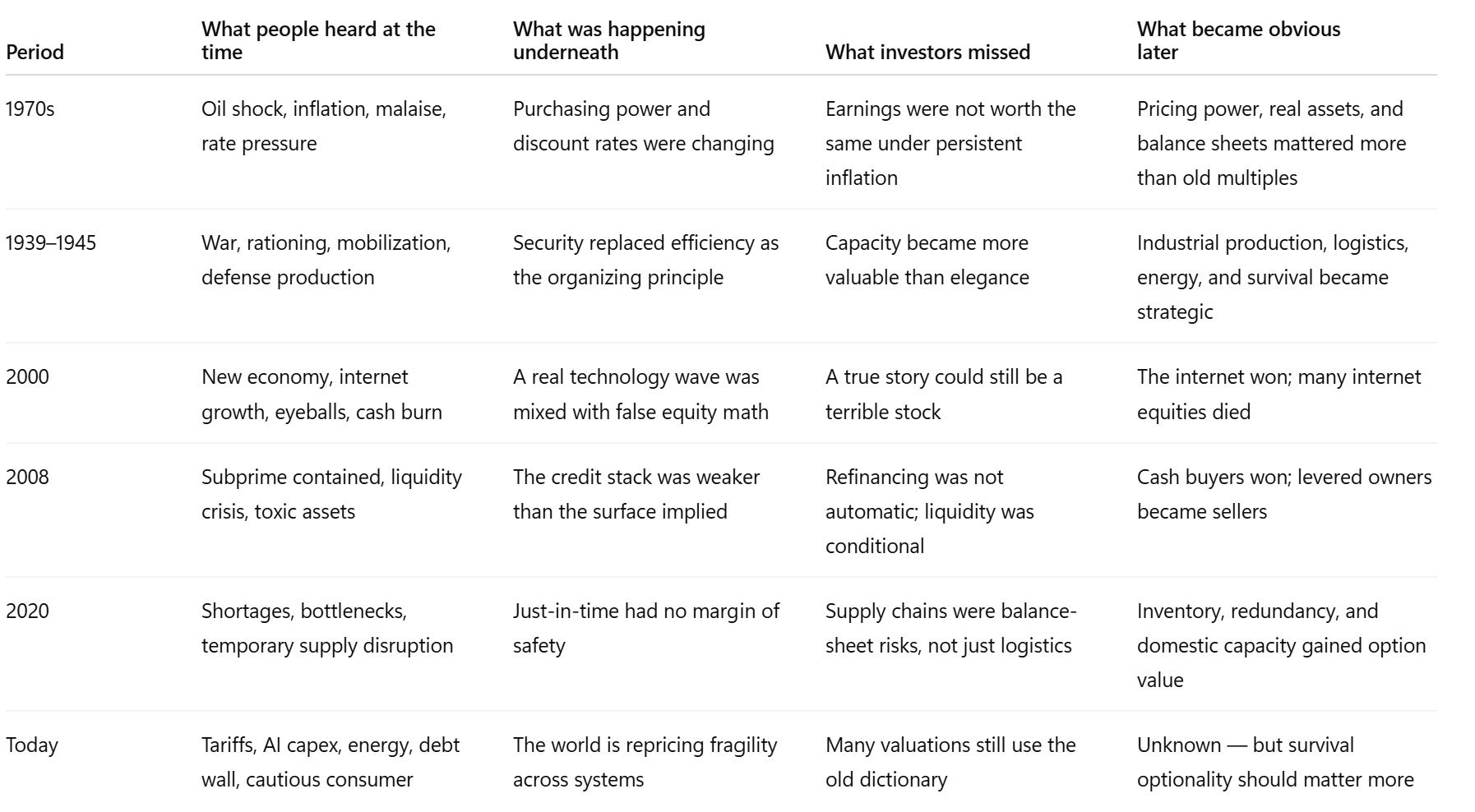

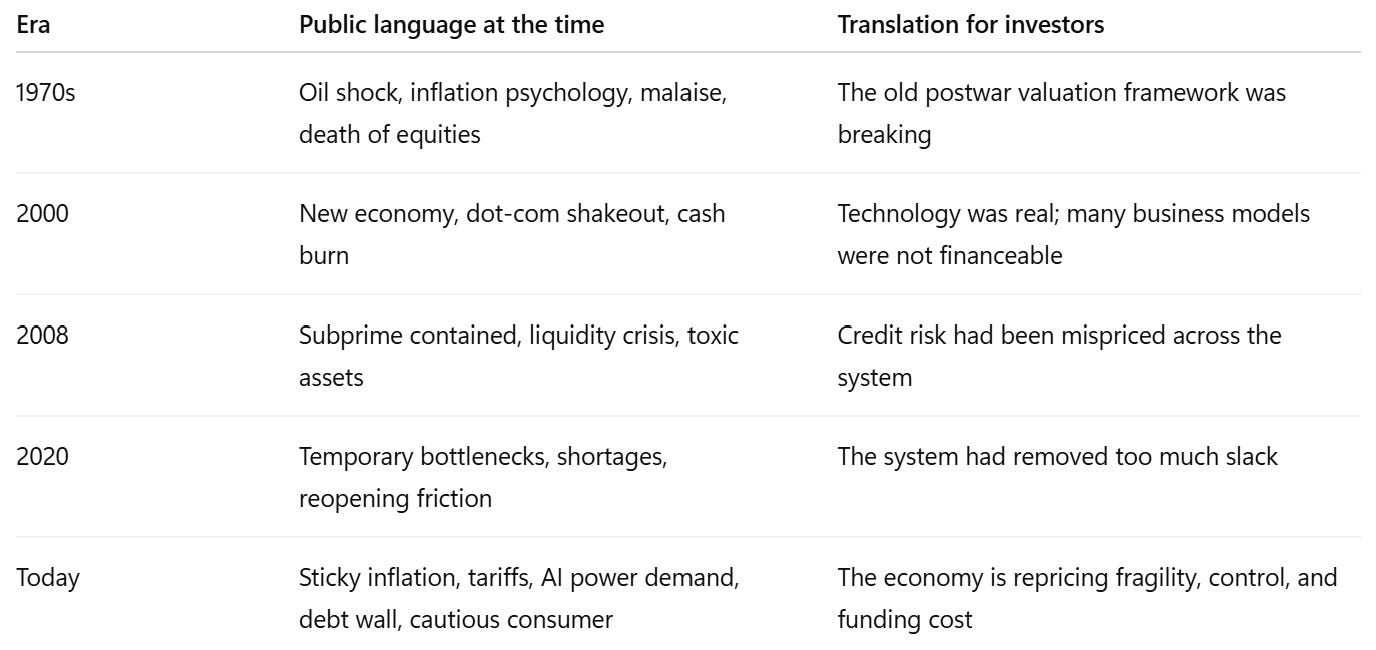

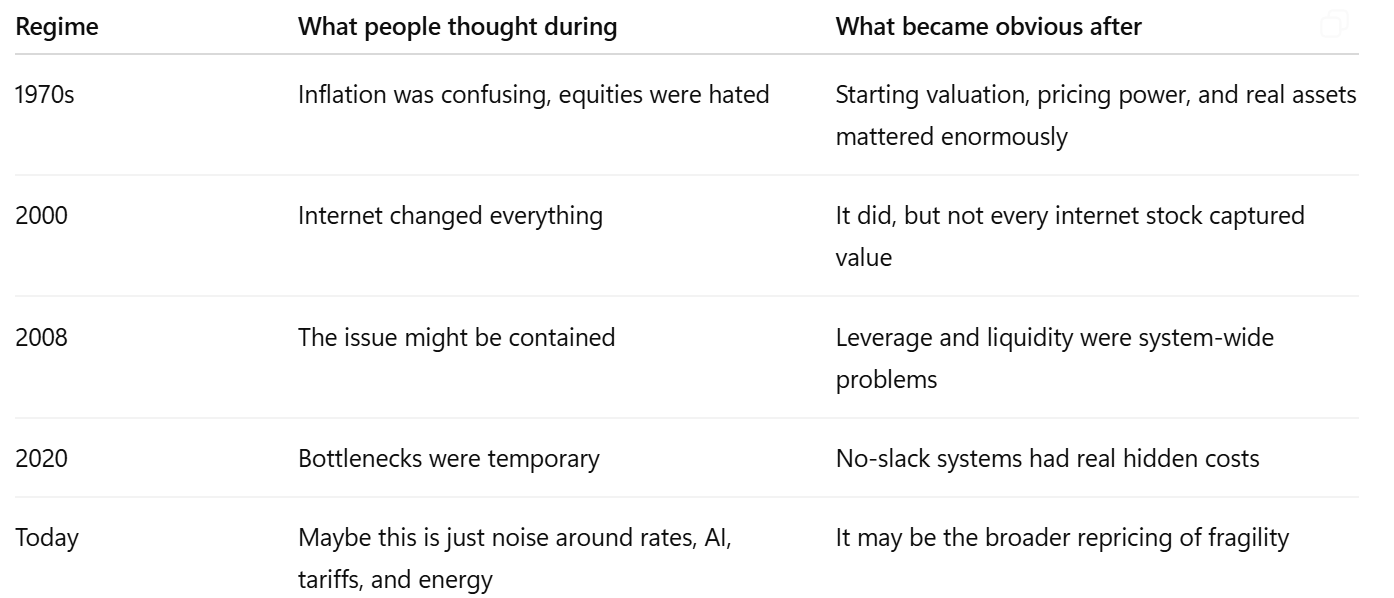

The 1970s rhyme is inflation and energy. The 2000 rhyme is real technology at the wrong price. The 2008 rhyme is refinancing and hidden leverage. The 2020 rhyme is supply chains without slack.

Today does not have to become any one of those periods. It can borrow pieces from all of them.

The useful question is not “which period is this?” That is for television. The better question is: what behavior is rhyming?

In every one of those periods, the old system trained people to ignore a specific risk. Then the regime changed, and that ignored risk became the story. In the 1970s, it was inflation and purchasing power. In 2000, it was cash burn and valuation. In 2008, it was credit structure. In 2020, it was supply-chain fragility.

Today, the ignored risk is wider: hidden leverage inside a world that used to feel frictionless.

A company can be levered through debt. That part is obvious. It can also be levered through one supplier, one country, one shipping lane, one energy input, one refinancing window, one customer cohort, one AI capex assumption, one grid constraint, one government policy, or one valuation multiple that only works when money is cheap.

The market understands financial leverage. It is still learning to price operational, geopolitical, and infrastructure leverage.

That is where some prices may still be using the old world.

Before the break, fragility looks smart

The cruel part is that fragility usually looks intelligent before it fails.

A company with no inventory looks efficient. A company with debt-funded buybacks looks disciplined. A country with no domestic industrial capacity looks rational because imports are cheaper. A retailer that squeezes suppliers looks sharp. A software company with no profit but huge growth looks visionary. A real estate company rolling short-term debt looks normal. A manufacturer dependent on one geography looks global. A consumer stretching payments looks confident.

Then the input changes. Rates rise. Energy moves. Trade gets political. Credit tightens. A supplier fails. A port closes. A government blocks exports. A war changes shipping routes. AI demand runs into physical bottlenecks. Suddenly the optimized system is not optimized anymore. It is exposed.

That’s why every regime shift humiliates the previous vocabulary. The words that sounded smart become evidence.

“Capital efficient” can become undercapitalized. “Lean” can become brittle. “Asset-light” can become asset-dependent without asset control. “Global scale” can become geopolitical exposure. “Adjusted earnings” can become weak cash generation. “Strategic transformation” can become a refinancing problem with better slides.

The words matter because they tell you what people are still trying to defend.

The news usually names the wrong thing first

During the transition, newspapers and television usually describe symptoms before structure. A regime shift is too large to name while it is happening, so the public conversation breaks it into smaller pieces.

The phrase “waiting for clarity” deserves special attention. It sounds responsible. It often means the old map has stopped working and the new one has not been accepted yet.

In the 1970s, the language eventually became exhaustion. Equities were not just down; they were hated. In 2000, the language was “new economy” until cash burn became impossible to ignore. In 2008, the language shifted from “contained” to “liquidity crisis.” The words changed because the system had already changed.

Today’s version is not identical, but the pattern is familiar. The public conversation keeps circling the same words: sticky inflation, energy shock, tariffs, AI capex, debt wall, cautious consumer, refinancing, resilience.

Those are not separate headlines. They are the economy discovering which assumptions are no longer free.

The public conversation wants one villain: oil, the Fed, tariffs, housing, AI, China, the consumer, commercial real estate. It is rarely that clean. The pressure usually comes from several places at once, and one pressure feeds the next.

Energy pushes inflation. Inflation pushes rates. Rates push refinancing. Refinancing pushes capital allocation. Capital allocation pushes layoffs and capex cuts. Layoffs feed consumer caution. Consumer caution feeds margins. Margins feed credit. Credit feeds equity. AI feeds power demand. Power demand feeds grid constraints. Grid constraints feed capex. Capex feeds balance sheets. Tariffs feed cost structure. Cost structure feeds pricing power. Pricing power feeds volume. Volume feeds profit. Profit feeds survival.

That is why the separate headlines belong in the same conversation.

People don’t collapse all at once

People talk about the consumer as if there are only two states: strong or weak. That is not how life works. The consumer usually adapts before he breaks.

He keeps spending, but changes the mix. He buys private label. He waits for promotions. He delays the car. He keeps the vacation but cuts the restaurant. He accepts one price increase but resists the next. He stretches payments. He keeps the job but worries about losing it. He says he is fine, but behaves like he is less fine than last year.

That matters because the income statement can still look okay while behavior underneath is changing. Revenue can rise because prices are higher. Same-store sales can hide unit pressure. Employment can look stable while hiring freezes. Credit losses can lag stress. Travel can remain strong while lower-income consumers are already tapped out. Management can say “resilient” while quietly increasing promotions.

Companies rarely say “the consumer is breaking” at first. They say the customer is selective, value-conscious, promotion-sensitive, prioritizing essentials, delaying discretionary purchases, or taking longer to decide.

Usually, it means people are still buying, but the purchase has become more conditional.They need the promotion. They need the payment plan. They need the cheaper option. They need the confidence that next month will not be worse.

This is the kind of market reading I want FRAGMENTS to do: not predicting the next headline, but noticing the change in behavior before it becomes obvious in the numbers.

Paid members get the deeper company work, balance-sheet maps, forced-seller setups, and deep-value reports behind that process.

Household debt: the psychology of the next payment

Debt is not just a balance-sheet item. It changes imagination.

A consumer with a low fixed mortgage, cheap auto loan, and rising wages thinks differently than a consumer facing higher rent, higher insurance, higher credit-card balances, higher grocery bills, and a job market that feels less forgiving. The next purchase gets judged against the next payment. That is the psychological channel.

This is why “resilient consumer” can be a dangerous phrase. It tells you the consumer has not stopped. It does not tell you how much stress has been absorbed to keep going.

A household does not become cautious only when it defaults. It becomes cautious when the buffer disappears. The emergency fund shrinks. The credit card balance stops feeling temporary. The car payment feels heavier. The mortgage rate locks the family in place. The raise no longer catches the grocery bill. The fear of losing a job becomes more important than the job itself.

That is the social layer of a regime shift. People keep participating, but the future gets smaller in their mind. Big purchases become decisions again. Debt stops feeling like convenience and starts feeling like someone else already owns part of the next paycheck.

Investors who only watch revenue miss this. The first sign is not always lower sales. It is lower tolerance: lower tolerance for price increases, lower tolerance for wait times, lower tolerance for bad service, lower tolerance for discretionary categories, lower tolerance for another monthly payment.

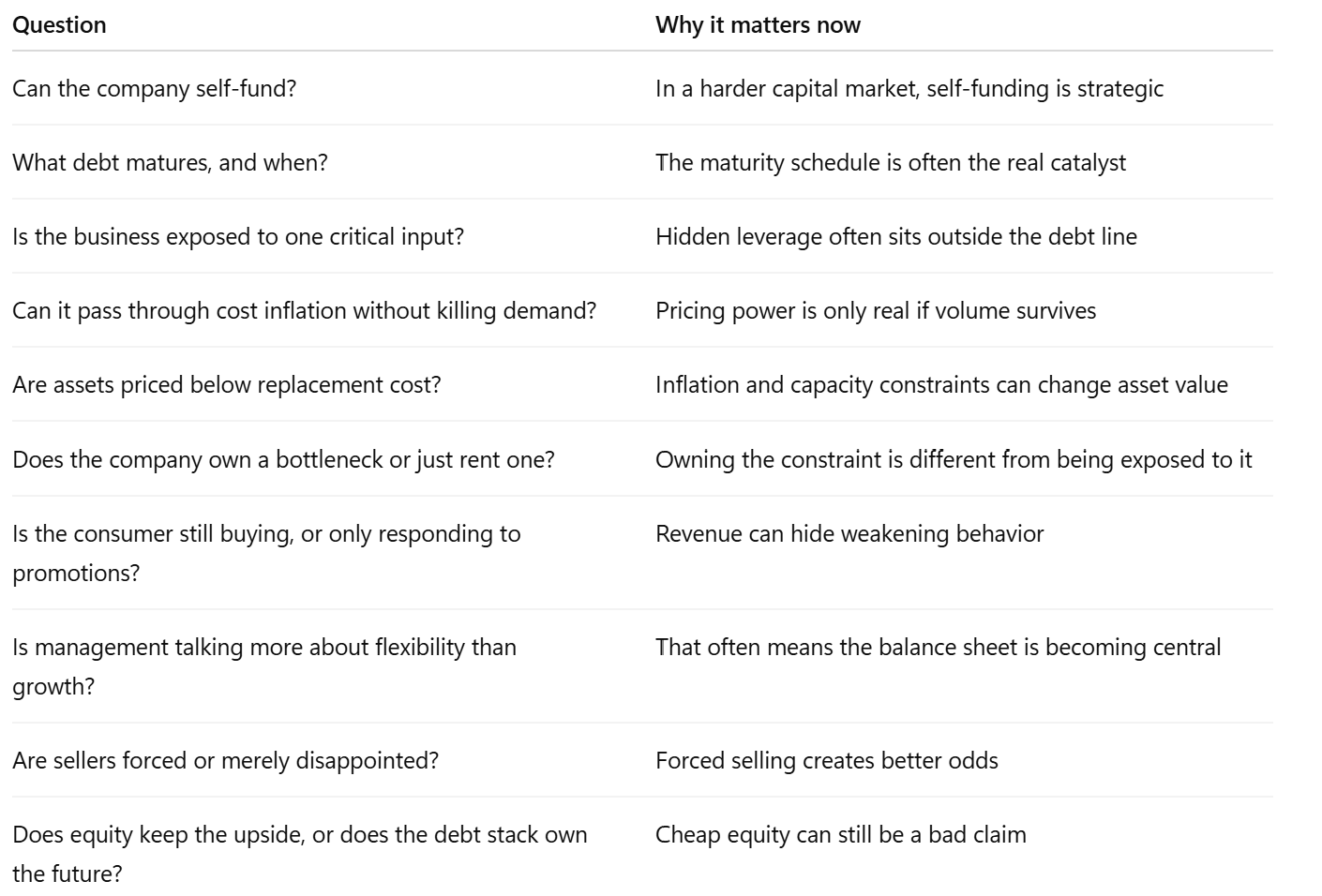

Corporate debt: the maturity schedule is the clock

For companies, the equivalent of the household payment is the maturity schedule.

The Fed is the weather. The maturity schedule is the clock.

A management team can talk about strategy, transformation, AI, market share, long-term demand, and normalized margins. Fine. But when debt comes due, the story meets the calendar. In the free-money world, refinancing was treated as a process. In a harder-money world, refinancing becomes an event.

In that kind of market, the presentation becomes less useful. Not useless, but less useful. Management can still explain the plan. The plan can even make sense. The problem is that the calendar may have its own plan.

A loan comes due. A coupon resets. A covenant gets closer. An asset that looked available for sale turns out to be more important than expected. A refinancing that used to feel automatic suddenly depends on lenders who have become more careful.

That is when the story changes tone. The company may still have assets. It may still have customers. It may still have a strategy. But if it needs outside money at the wrong moment, the stock is no longer just about the business. It is about time, the debt, and who gets to make the next decision.

When money was cheap, a lot of companies could keep the story going. Growth covered the weak balance sheet. Refinancing was treated like paperwork. Nobody spent much time on the maturity schedule because the market was usually open.

That changes when money costs more. Debt stops being a footnote and starts setting the calendar.

So “cheap” is not enough. Cheap for whom? Common shareholders? Lenders? A buyer of the whole company? If the creditors own the next decision, the equity may not be cheap at all. It may just be the last piece of a structure that needs new money.

The best investors get there before the screen does. They are not asking only how far the stock has fallen. They are asking how much time the equity still owns.

Geopolitics is entering the cost structure

A few years ago, many investors could treat geopolitics as something that happened outside the model. It moved oil for a week, hurt sentiment for a quarter, and then the spreadsheet went back to normal.

That is harder to do now.

A tariff is not just a headline. It changes the landed cost of a product. An export control can force a redesign. A shipping route can change inventory needs. A defense budget can pull labor and materials into one part of the economy and away from another. Energy risk can move from the commodity screen into freight, food, aviation, chemicals, utilities, and household budgets.

Tariffs are gross margin, supplier choice, pricing power, inventory planning, and consumer elasticity. Energy risk is freight, petrochemicals, utilities, food, aviation, mining, manufacturing, and household budgets. Export controls are production delays, redesign costs, supplier concentration, and strategic inventory. Defense spending is fiscal allocation, industrial capacity, labor demand, materials demand, and opportunity cost. Shipping lanes are delivery times, insurance costs, working capital, and customer reliability. Critical minerals are permitting, capex, geopolitical dependency, replacement cost, and the speed at which the energy and AI buildout can happen.

That is the real change. Politics is no longer sitting outside the model. It is moving into the model.

For a long time, investors could treat geopolitics as episodic noise unless they owned obviously exposed assets. Now it touches cost structures across sectors. A company can have no flag in the headline and still be exposed through inputs, shipping, energy, labor, financing, or customers.

The market will keep asking, “Is this geopolitical event contained?” The better question is, “Which cost assumptions changed even if the event is contained?”

AI still needs electricity

AI makes this entire regime stranger because it looks weightless from the outside and extremely physical underneath.

The surface story is intelligence, software, automation, productivity. The underside is chips, power, cooling, land, water, copper, gas, transformers, substations, permits, transmission, and capex. The market wants to debate whether AI is a bubble. That is not the best question. The best question is who captures the economics after the physical bottlenecks and capital cycle respond.

In 2000, the internet was real and still destroyed plenty of equity capital. The lesson was not that the technology was fake. The lesson was that a true technology does not repeal price, funding, competition, or capital intensity.

Today’s AI cycle rhymes with 2000, but with a twist. The supposedly digital revolution is pulling value back toward physical constraints. If power is scarce, the grid matters. If chips are scarce, supply chains matter. If data centers need enormous capital, financing matters. If everyone builds capacity at once, future returns may compress. If the obvious winners are already priced as obvious winners, the investor has to look elsewhere or wait.

The question is not whether AI matters. It does. The question is who makes the money after the spending is done, and how much of that future is already in the stock.

In 2000, the internet changed the world. That did not make every internet stock a good investment. Same rule here.

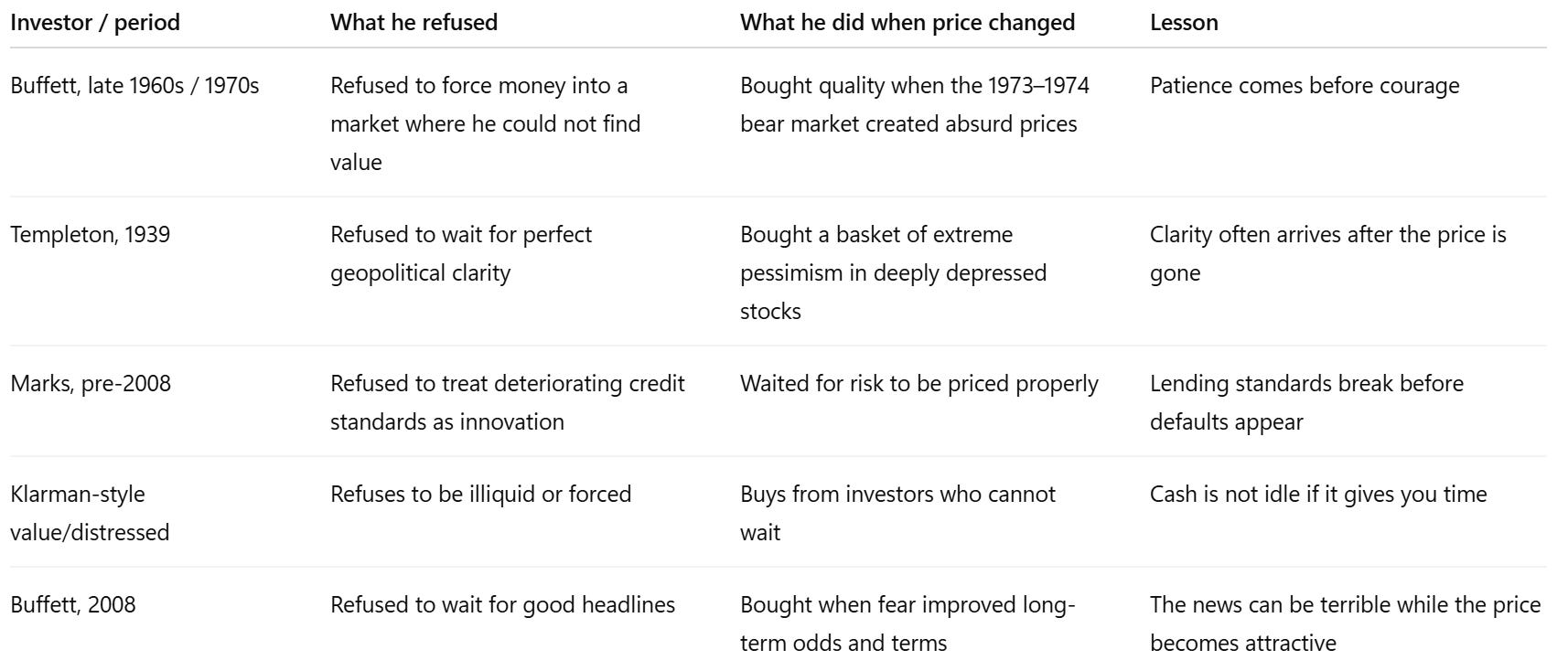

What great investors refused to do

Good investors are usually remembered for what they bought. The quieter lesson is what they refused to buy.

They did not need the perfect macro forecast. They needed a price that gave them room to be wrong and a balance sheet that gave them time.

Some things are cheap because people are tired of looking at them. Others are cheap because the business has been damaged. The work is knowing which is which.

The pattern is not prediction. It is refusal.

Refusal to chase when the price is wrong. Refusal to call bad credit innovation. Refusal to confuse a real technology with a good investment. Refusal to need perfect clarity before acting. Refusal to be the investor who needs capital at the same time everyone else does.

That is the useful part now. The market does not reward the person who can describe the regime change after it happens. It rewards the person who can stay liquid, stay patient, and recognize when fear has finally changed the price.

What people say before the obvious becomes obvious

After every crisis, people say the warning signs were clear. They were not. Or more precisely, they were clear only to people looking in the right place.

Before 2000 broke, the public conversation was not “this is a cash-flow problem.” It was “new economy.” The better investors were asking who needed capital and whether the business model could fund itself.

Before 2008 broke, the public conversation was not “the entire credit system is mispriced.” It was “subprime may be contained.” The better investors were asking who owned the risk, how much leverage was embedded, and what happened if refinancing stopped.

Before the 1970s became obvious, investors were not all calmly preparing for inflation. Many were still using old valuation habits. The better investors were asking which businesses had pricing power, which assets held real value, and which securities were priced for despair.

Before 2020 exposed supply chains, many companies treated just-in-time as pure efficiency. The better question would have been: what is the cost of no slack when the system stops?

Today’s version is similar. The public conversation says sticky inflation, tariffs, AI capex, energy volatility, cautious consumers, and debt walls. The better question is: where is the hidden leverage?

The debt line is only one place to look. Sometimes the real pressure is elsewhere: a supplier the company cannot replace quickly, a country it depends on too much, a shipping route that has become less reliable, a refinancing date that arrives at the wrong time, a customer group that has less room to spend, or a cost assumption that quietly carried the margin.

Those things do not look like leverage in a normal year. Then the conditions change, and suddenly they do.

The line: efficiency without resilience is leverage

This is the sentence that holds the whole article together:

Efficiency without resilience is leverage by another name.

A company that removes every buffer is making a bet. It may not show up as debt, but it is leverage. A manufacturer with one critical supplier is levered. A retailer with no inventory cushion is levered. A country with no domestic capacity in strategic inputs is levered. A data-center boom that assumes unlimited power is levered. A consumer company that assumes endless pricing power is levered. A real estate company that assumes refinancing is automatic is levered. A software story that assumes capital markets will keep funding growth is levered.

This is why the old efficiency premium is being challenged. The world is not saying efficiency no longer matters. It is saying efficiency without backup has a cost.

That cost was underpriced for years.

Now it is being repriced.

The market is slowly learning to pay for things it used to call waste: inventory, redundancy, spare capacity, cash, domestic production, energy access, physical bottlenecks, low leverage, and time.

But this is where the analysis has to stay honest. Not every hard asset is good. Not every domestic manufacturer is strategic. Not every utility is cheap. Not every defense contractor is attractive. Not every commodity stock is a hedge. Not every low-multiple stock is mispriced. A bad asset with a patriotic story is still a bad asset. A levered company with “resilience” in the deck is still levered.

The interesting part is not the theme itself. By the time a theme has a name, a lot of people already own it.

The better question is where the market is still using old assumptions. Maybe it is treating inventory as waste when it has become protection. Maybe it is discounting a physical asset without checking replacement cost. Maybe it is calling a cash-rich company lazy when that cash gives management room to buy from weaker competitors. Maybe it is calling an equity cheap without noticing that the debt schedule has already taken control.

That is where the work is.

What this makes us look for

Higher defense spending does not make every defense stock attractive. More power demand does not make every utility cheap. AI infrastructure can be real and still be overpaid for. Energy risk can matter without making every energy stock a bargain.

A theme only tells you where to look. It does not tell you what to pay, who controls the balance sheet, how much capital is needed, or whether management is any good.

That part still has to be done one company at a time.

The question is simple: what does the headline actually change in the business?

It is slower work. It does not sound good on television. But it is usually where the answer is: debt, cash, assets, customers, and price.

What we would not touch casually

The same logic also tells you what to leave alone.

I would be careful with any company that needs cheap refinancing to make the equity work. I would be careful with businesses where “resilience” appears in the presentation but the debt schedule says something else. I would be careful with AI beneficiaries where the story is real but the price already assumes victory. I would be careful with consumer companies where revenue growth is mostly price, promotions are rising, and units are weakening underneath.

The most dangerous stocks in this kind of market are not always the expensive ones. Sometimes they are the cheap ones that only looked cheap under the old rules.

Some cheap stocks are not mispriced. They are just priced for a world that is gone.

Where the market may be wrong now

The market will not get this right everywhere at the same time. Some of the obvious winners are probably already crowded. Some companies with the right words in the deck are already priced as if nothing can go wrong. I would not assume that is where the best risk/reward still sits.

The better work is in the awkward places. A company carrying more inventory than investors like, but doing it for a reason. A physical asset the market still values like yesterday’s problem, even though replacement cost has moved. A business with cash that looks lazy until weaker competitors need money. A domestic plant that looked subscale when imports were easy, but looks different when lead times, tariffs, and reliability matter. A stock that screens cheap, but is really just waiting on lenders.

None of that can be solved with a theme. It has to be done name by name. What is real? What is just language? What is protected by the balance sheet? What needs outside money? What is merely hated, and what is actually broken?

That is where most people stop. It is also where the work starts.

What happens after

Later, the story always looks cleaner than it felt at the time.

People look back and say the signs were obvious. Inflation changed the multiple. Internet companies needed cash. Housing was more levered than advertised. Supply chains had no spare room. Power demand was going to matter. Refinancing was going to be harder.

But that is not how it feels while it is happening. While it is happening, there are good arguments on both sides. The data is mixed. The old winners still look strong. The first cracks can be explained away. People who sell early look foolish. People who buy early look worse.

That is why prices move. Not because nobody sees it, but because most people wait until it is safe to say it out loud.

We will probably describe this period better later. That is how it usually works.

Maybe the market understood AI before it understood the power bill. Maybe it saw the growth before it saw the financing. Maybe it kept valuing efficiency long after the world had become less forgiving.

By the time the sentence sounds obvious, the price will probably have moved.

Bottom line

This period will probably make more sense later than it does now. Most of them do.

We can already see the pieces: inflation and energy from the 1970s, security over efficiency from the wartime economy, real technology at dangerous prices from 2000, liquidity and refinancing from 2008, and supply chains without slack from 2020. None of those comparisons is perfect. They do not need to be.

The point is not that history repeats. The point is that markets keep forgetting the same types of risk when the world feels easy.

This time, the forgotten risk is resilience. Companies built for cheap capital, smooth supply chains, predictable energy, easy imports, generous consumers, and friendly refinancing are being asked harder questions. Some will answer them. Some will not.

The words have already changed. Consumers are more careful. CEOs talk more about flexibility. Governments talk more about capacity. Investors talk more about maturities. That does not mean everything breaks. It means the market has to put a new price on things it used to treat as background.

The best investors do not need the perfect headline. They need to know who has time, who needs money, who is being forced to sell, and what price gives enough room to be wrong.

Most people will wait until the new language feels obvious. By then, the better investors are usually somewhere else: reading the balance sheet, watching the customer, studying the debt schedule, and buying what the market is too tired to understand.

That is the rhyme.

If this is the kind of market reading you want every week, join FRAGMENTS.

Paid members get the deeper company work: balance-sheet maps, forced-seller setups, deep-value reports, and the watchlists built from this work.

I enjoyed this piece.

The idea that regime shifts first appear in vocabulary rather than in headline statistics struck me as particularly insightful.

One thing I found myself wondering while reading is whether some forms of fragility originate outside the balance sheet entirely.

The essay does an excellent job tracing financial, operational, energy, supply-chain, and refinancing vulnerabilities. But increasingly I find myself asking whether institutions and public attitudes can become sources of fragility as well.

For example, AI infrastructure may appear financially viable, yet still encounter resistance from regulators, local communities, labor markets, or political systems. The vulnerability is real, but it doesn't necessarily originate in the company's financial structure.

Perhaps those pressures eventually show up in the balance sheet. But they seem to emerge elsewhere first.

That made me wonder whether some of the vocabulary shifts you describe are not only signals of economic change, but signals that institutions themselves are beginning to renegotiate the assumptions underlying the system.