Reflexivity—when markets stop observing reality, and start creating it

George Soros did not argue that the markets are always irrational; he also did not argue that there is no objective reality.

He simply took a much more nuanced position. People in the markets don’t ever perceive the world perfectly. They act based on a combination of their perceptions (which are incomplete or warped) and how they behave. Those behaviors can, in turn, alter the very reality they were attempting to understand.

Soros presented these ideas using the concepts of fallibility and reflexivity. In a simplistic manner:

perceptions alter prices

prices alter behavior

behavior alters realities

Most people who hear “reflexivity,” immediately relate it to bubbles. A stock price rises due to investor perception. That increasing price gives the issuing entity the opportunity to raise additional capital, expand operations, acquire competing companies, etc., thereby reinforcing the original perception.

That is one type of reflexivity.

However, at present, that is the least significant form of reflexivity.

The more significant form of reflexivity arises from the process where a real-world shock occurs and market reactions to that shock begin to magnify the impact of that shock. At that moment, the market ceases to be merely a scorekeeper, and instead becomes a mechanism to shape its own reality.

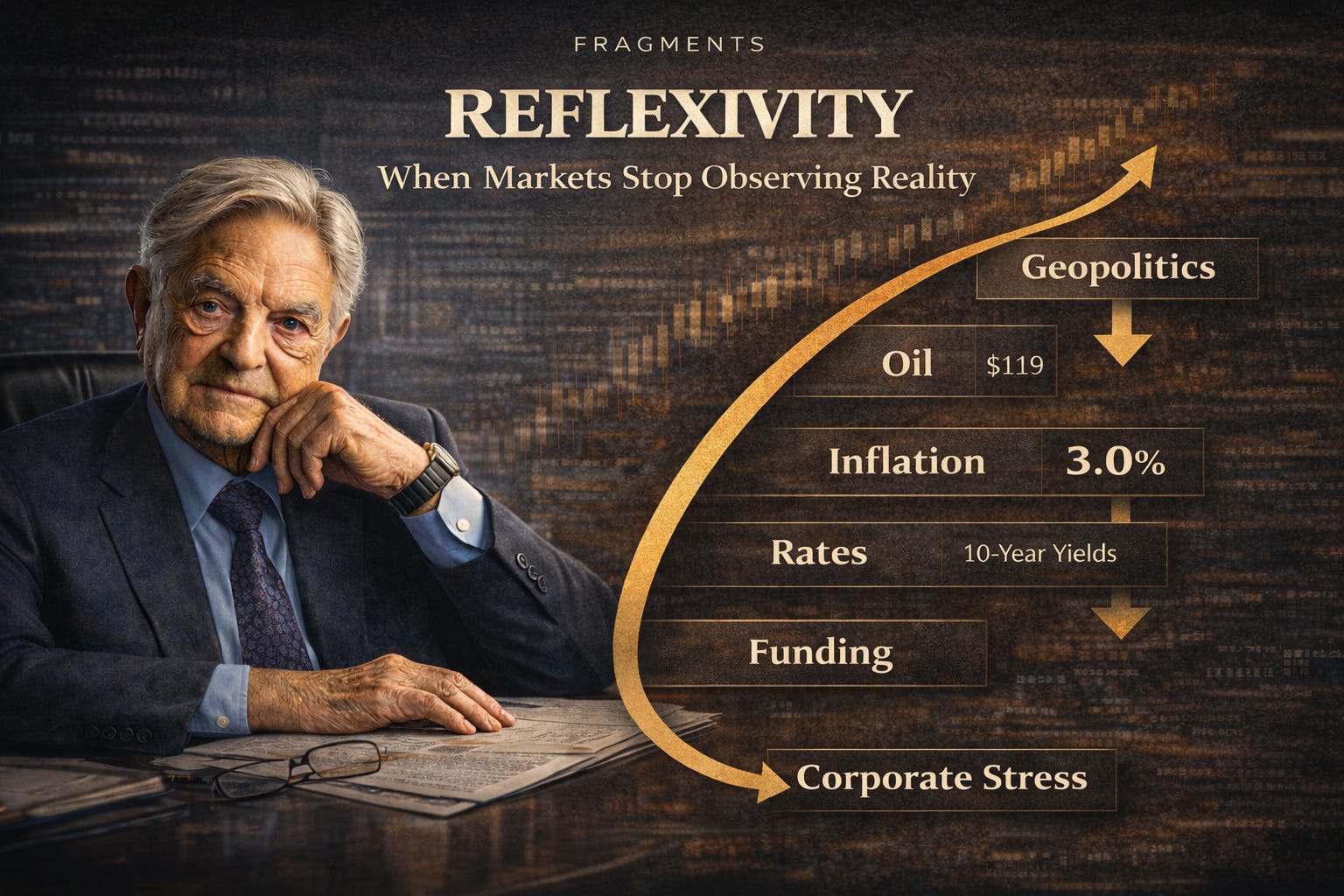

At this writing (March 2026), the escalating conflict with Iran has caused Brent crude to reach an intra-day price of $119.50, and has precipitated a sell-off in global bonds as investors re-price inflation risk. The IMF has cautioned that a sustained 10% increase in the price of oil will contribute approximately 0.4% to global inflation.

This is not merely an occurrence—it is a reflexive chain reaction.

Moreover, the fundamental insight regarding this particular example is:

markets do not merely price reality—they aid in creating the next iteration of it.

Prior to Reflexivity, There Was a Trigger

The biggest mistake made in the analysis of markets is assuming that every shock must arise from some form of economic weakness.

That was not the case in this instance. Prior to the geopolitical deterioration, the global economy had not collapsed. The IMF had forecasted 3.3% global GDP growth for 2026. The world was not perfect by any means, however it was operating; growth had not ceased; trade had not stopped; and markets had not broken.

Then the trigger occurred. Tensions surrounding Iran’s nuclear program had escalated diplomatically. Militarization of positions had been initiated. The conflict began spreading throughout the region.

Instantly, markets were no longer concerned with hypothetical geopolitical risk. Markets were concerned with the actual energy disruption risk.

At this point, the process of reflexivity commences.

The first cause of this particular chain was geopolitical. However, the financial and economic consequences that markets are responding to today are a result of the effects of their responses. Once those responses feed back into pricing, funding, and behavior, the feedback loop begins to build upon itself.

Why did the Shock spread so fast?

The Shock moved rapidly for a simple reason: the system was vulnerable to the wrong things already.

Sensitive to:

• energy prices

• Inflation

• interest rates

• financial plumbing

All modern financial systems do not absorb shocks slowly. They transmit them.

When Oil spikes, the Shock is transmitted rapidly out of commodity Markets.

Oil goes up.

Expectations of Inflation go up.

Yields on bonds adjust.

Funding costs change.

Corporate decisions shift.

At that point, the market is no longer observing the event; the market’s reaction is contributing to the event.

That is reflexivity in action: the Trigger lights the fire, and market behavior spreads the fire.

The Reflexivity Chain

Once you strip down the mechanism, it is really quite straightforward.

Geopolitical Trigger

↓

Oil prices spike

↓

Inflation expectations rise

↓

Bond yields rise

↓

Funding conditions tighten

↓

Fear increases

↓

Credit spreads widen

↓

Stress increases

↓

Fear reinforces itself

That is the loop.

As soon as it starts, Markets are no longer just reacting to the original Shock; Markets are amplifying the Shock through funding conditions, pricing behavior, and rising Stress across the system.

Reflexivity is really a theory of Transmission.

Layer one -- Geopolitics: when Fear becomes cost

Geopolitics becomes economically significant when it changes real world flows.

The Transmission channel is clear:

War risk increases

Shipping risk increases

Risk to energy supply increases

Oil price goes up

Inflation expectations go up

A missile does not need to hit your factory to damage your business. It only needs to disrupt tanker routes, raise insurance premiums, and increase fuel costs.

That is the moment when Geopolitics ceases to be foreign policy and becomes an operating cost. And as soon as operating costs rise across an Economy, Inflation expectations begin to adjust.

That is when Geopolitics enters the realm of macroeconomics.

Layer Two -- Macro: when funding conditions become the Economy

Most Macro commentaries have focused on macroeconomic variables (cpi, gdp, employment, central banks), etc.

These matter. However, the larger question is simpler:

Who can fund themselves at what price with how much confidence behind them?

Currently, that answer is changing.

When energy prices jump and Inflation expectations rise, Bond investors demand more compensation. Yields move higher. And when yields rise, the cost of money also rises.

This changes behavior across the system:

Issuers delay borrowing.

Borrowers hedge more aggressively.

Lenders tighten lending standards.

Investors demand wider spreads.

Management teams plan for a tougher environment.

Thus, macroeconomics is not just a background.

Macroeconomics is the funding environment.

It is important not to force the wrong conclusion here. If Inflation risk is increasing because Oil is increasing, then the immediate pressure on rates is positive (not negative).

Lower rates usually belong to a different regime:

When the energy Shock fades

When growth weakens sharply

Or when Markets shift from Inflation Fear to recession Fear

Knowing which reflexive loop we are in matters a great deal. If you misread the loop, you misread the market.

Layer Three -- micro: when Markets start to change Companies

Reflexivity is most visible at the company level.

A lower share price reduces strategic flexibility.

A wider credit spread raises refinancing costs.

Higher energy costs compress margins.

A less favorable funding climate changes what management can realistically do.

Companies are not independent of Markets. Markets change the conditions under which Companies operate.

Thus, many businesses are no longer operating under an earnings narrative. They are operating under a financing narrative.

Micro example 1 -- airlines

Airlines are an easy example.

Oil jumps. Fuel costs jump. Margins come under pressure. Earnings expectations fall. Credit spreads widen. Refinancing becomes more expensive. Equity prices fall. Strategic flexibility falls.

Nothing mystical happened there. The market reaction made the problem harder to manage.

That is reflexivity.

Micro example 2 -- commercial real estate

Commercial real estate shows the same mechanism even more violently.

When interest rates rise, refinancing costs rise and lenders tighten their standards. Property owners struggle to refinance, asset prices decline, market confidence declines, and funding becomes harder.

The buildings did not get worse suddenly.

What changed was the financial environment around them. And as soon as the environment changed, valuations stopped being abstract and became conditional.

Micro example 3 -- deep Value Stocks

Deep Value Stocks are often misunderstood.

They are not cheap. They are trapped in a negative reflexive loop:

Low price

Negative narrative

Limited access to capital

Reduced strategic flexibility

More skepticism in the market

Even lower price

That is not just sentiment. That is a shrinking field of possibilities.

However, reflexive loops can reverse:

Debt gets refinanced

Asset sale reduces leverage

Cash flow stabilizes

Deadline feared passes without disaster

The market stops pricing inevitability. And that is where reratings typically begin.

What actually created this reflexive moment

Markets love single-cause explanations, but reality is rarely that simple.

The cause was not war alone. Nor was it Oil prices alone. Nor was it economic weakness alone.

The true explanation is layered.

A geopolitical event hits a global system still growing but extremely sensitive to energy, Inflation, and funding conditions. Markets then started repricing not only the original event, but also the second- and third-order consequences of that event.

The chain looks like this:

Trigger — conflict escalates

Translation — energy/freight risk increases

Repricing — Inflation expectations increase

Transmission — Bond yields adjust

Outcome — funding conditions tighten

That is the reflexive chain.

The first cause was geopolitical. The second cause was market behavior. And the third cause, if this continues to play out, may be financial Stress itself.

What could create the Next Reflexive Loop

Understanding reflexivity is not just about explaining the present. It is about identifying the next regime before it fully forms.

There are Three main paths.

Scenario 1 -- the current loop strengthens

If Oil remains high and Inflation expectations remain elevated, Bond yields will continue to come under pressure and funding conditions will tighten further.

The chain looks like this:

High energy

Persistent Inflation

Higher yields

Tighter credit

Corporate Stress

This path presents the greatest danger to leveraged balance sheets, refinancing-dependent industries and Companies that relied on generous capital Markets.

Scenario 2 -- Stress enters financial plumbing

Eventually, attention may shift from Inflation to liquidity.

The loop could look like this:

Macro-Stress

Liquidity Stress

Widening credit spreads

Forced sales of assets

Increased instability in the market

This is often the ugly phase. It is also the phase where assets that already appear cheap can get cheaper before real opportunities show up.

Scenario 3 -- the loop reverses

The final scenario is reversal.

If energy supply risks decline or policy intervention stabilizes Markets, the chain can flip:

Oil decreases

Decrease in Inflation expectations

Decrease in Bond yields

Easing of funding conditions

Risk assets recover

That does not fix weak businesses overnight. But it does reduce the pressure of financing sitting on top of them. In many cases, that is enough to change the narrative.

Signals that tell us which direction the system is taking

Several signals can tell us which path the system has taken.

first, whether Oil prices remain elevated or begin to fall.

second, whether Inflation expectations continue to rise.

third, whether Bond yields remain under pressure or begin to stabilize.

Fourth, whether policymakers begin to emphasize financial stability rather than fighting Inflation.

Fifth, whether corporate refinancing becomes difficult and dominates discussion in Markets.

If Oil falls, the chain begins to unwind.

If yields remain high, funding remains under pressure.

If refinancing becomes the central issue, the problem has moved from Markets to Companies.

What causes the reflexivity loop to stop

Reflexive systems do not run indefinitely. At some point something interrupts the chain.

In the current environment several things can do that.

1. Oil prices stabilize

If energy stoppages cease, Inflation expectations will cool. When Inflation expectations fall, Bond yields will stabilize. And when yields stabilize, the chain begins to unwind.

2. Policymakers change priorities

If central banks and governments focus from fighting Inflation to protecting financial stability, funding conditions will ease. Liquidity will return. The loop will lose power.

3. Markets adapt

Sometimes the system adapts. Companies hedge energy exposure, supply chains reroute, inventories normalize and the same headlines will no longer produce the same Fear response.

The loop does not end when Fear goes away. It ends when Fear stops creating the same scale of behavior in the system.

Conclusion

Reflexivity is not merely a theory regarding bubbles. Reflexivity is a framework for understanding how pressures move through the system.

A geopolitical event becomes an energy event.

An energy event becomes an Inflation event.

An Inflation event becomes a rate event.

A rate event becomes a funding event.

A funding event becomes a corporate event.

Markets are not simply observing events. Markets are amplifying those events. And sometimes helping determine what those events become.

In reflexive systems, price does not only describe reality. Price helps create it.

Markets do not travel in straight lines. Markets travel in loops. And the most important loops are often invisible until they have already shaped the system.

A geopolitical event becomes energy Stress.

Energy Stress becomes Inflation pressure.

Inflation pressure becomes funding pressure.

Funding pressure becomes reality for corporations.

That is reflexivity.

Why did the Shock spread so fast?

The Shock moved rapidly for a simple reason: the system was vulnerable to the wrong things already.

Sensitive to:

• energy prices

• Inflation

• interest rates

• financial plumbing

All modern financial systems do not absorb shocks slowly. They transmit them.

When Oil spikes, the Shock is transmitted rapidly out of commodity Markets.

Oil goes up.

Expectations of Inflation go up.

Yields on bonds adjust.

Funding costs change.

Corporate decisions shift.

At that point, the market is no longer observing the event; the market’s reaction is contributing to the event.

That is reflexivity in action: the Trigger lights the fire, and market behavior spreads the fire.

The Reflexivity Chain

Once you strip down the mechanism, it is really quite straightforward.

Geopolitical Trigger

↓

Oil prices spike

↓

Inflation expectations rise

↓

Bond yields rise

↓

Funding conditions tighten

↓

Fear increases

↓

Credit spreads widen

↓

Stress increases

↓

Fear reinforces itself

That is the loop.

As soon as it starts, Markets are no longer just reacting to the original Shock; Markets are amplifying the Shock through funding conditions, pricing behavior, and rising Stress across the system.

Reflexivity is really a theory of Transmission.

Layer one -- Geopolitics: when Fear becomes cost

Geopolitics becomes economically significant when it changes real world flows.

The Transmission channel is clear:

War risk increases

Shipping risk increases

Risk to energy supply increases

Oil price goes up

Inflation expectations go up

A missile does not need to hit your factory to damage your business. It only needs to disrupt tanker routes, raise insurance premiums, and increase fuel costs.

That is the moment when Geopolitics ceases to be foreign policy and becomes an operating cost. And as soon as operating costs rise across an Economy, Inflation expectations begin to adjust.

That is when Geopolitics enters the realm of macroeconomics.

Layer Two -- Macro: when funding conditions become the Economy

Most Macro commentaries have focused on macroeconomic variables (cpi, gdp, employment, central banks), etc.

These matter. However, the larger question is simpler:

Who can fund themselves at what price with how much confidence behind them?

Currently, that answer is changing.

When energy prices jump and Inflation expectations rise, Bond investors demand more compensation. Yields move higher. And when yields rise, the cost of money also rises.

This changes behavior across the system:

Issuers delay borrowing.

Borrowers hedge more aggressively.

Lenders tighten lending standards.

Investors demand wider spreads.

Management teams plan for a tougher environment.

Thus, macroeconomics is not just a background.

Macroeconomics is the funding environment.

It is important not to force the wrong conclusion here. If Inflation risk is increasing because Oil is increasing, then the immediate pressure on rates is positive (not negative).

Lower rates usually belong to a different regime:

When the energy Shock fades

When growth weakens sharply

Or when Markets shift from Inflation Fear to recession Fear

Knowing which reflexive loop we are in matters a great deal. If you misread the loop, you misread the market.

Layer Three -- micro: when Markets start to change Companies

Reflexivity is most visible at the company level.

A lower share price reduces strategic flexibility.

A wider credit spread raises refinancing costs.

Higher energy costs compress margins.

A less favorable funding climate changes what management can realistically do.

Companies are not independent of Markets. Markets change the conditions under which Companies operate.

Thus, many businesses are no longer operating under an earnings narrative. They are operating under a financing narrative.

Micro example 1 -- airlines

Airlines are an easy example.

Oil jumps. Fuel costs jump. Margins come under pressure. Earnings expectations fall. Credit spreads widen. Refinancing becomes more expensive. Equity prices fall. Strategic flexibility falls.

Nothing mystical happened there. The market reaction made the problem harder to manage.

That is reflexivity.

Micro example 2 -- commercial real estate

Commercial real estate shows the same mechanism even more violently.

When interest rates rise, refinancing costs rise and lenders tighten their standards. Property owners struggle to refinance, asset prices decline, market confidence declines, and funding becomes harder.

The buildings did not get worse suddenly.

What changed was the financial environment around them. And as soon as the environment changed, valuations stopped being abstract and became conditional.

Micro example 3 -- deep Value Stocks

Deep Value Stocks are often misunderstood.

They are not cheap. They are trapped in a negative reflexive loop:

Low price

Negative narrative

Limited access to capital

Reduced strategic flexibility

More skepticism in the market

Even lower price

That is not just sentiment. That is a shrinking field of possibilities.

However, reflexive loops can reverse:

Debt gets refinanced

Asset sale reduces leverage

Cash flow stabilizes

Deadline feared passes without disaster

The market stops pricing inevitability. And that is where reratings typically begin.

What actually created this reflexive moment

Markets love single-cause explanations, but reality is rarely that simple.

The cause was not war alone. Nor was it Oil prices alone. Nor was it economic weakness alone.

The true explanation is layered.

A geopolitical event hits a global system still growing but extremely sensitive to energy, Inflation, and funding conditions. Markets then started repricing not only the original event, but also the second- and third-order consequences of that event.

The chain looks like this:

Trigger — conflict escalates

Translation — energy/freight risk increases

Repricing — Inflation expectations increase

Transmission — Bond yields adjust

Outcome — funding conditions tighten

That is the reflexive chain.

The first cause was geopolitical. The second cause was market behavior. And the third cause, if this continues to play out, may be financial Stress itself.

What could create the Next Reflexive Loop

Understanding reflexivity is not just about explaining the present. It is about identifying the next regime before it fully forms.

There are Three main paths.

Scenario 1 -- the current loop strengthens

If Oil remains high and Inflation expectations remain elevated, Bond yields will continue to come under pressure and funding conditions will tighten further.

The chain looks like this:

High energy

Persistent Inflation

Higher yields

Tighter credit

Corporate Stress

This path presents the greatest danger to leveraged balance sheets, refinancing-dependent industries and Companies that relied on generous capital Markets.

Scenario 2 -- Stress enters financial plumbing

Eventually, attention may shift from Inflation to liquidity.

The loop could look like this:

Macro-Stress

Liquidity Stress

Widening credit spreads

Forced sales of assets

Increased instability in the market

This is often the ugly phase. It is also the phase where assets that already appear cheap can get cheaper before real opportunities show up.

Scenario 3 -- the loop reverses

The final scenario is reversal.

If energy supply risks decline or policy intervention stabilizes Markets, the chain can flip:

Oil decreases

Decrease in Inflation expectations

Decrease in Bond yields

Easing of funding conditions

Risk assets recover

That does not fix weak businesses overnight. But it does reduce the pressure of financing sitting on top of them. In many cases, that is enough to change the narrative.

Signals that tell us which direction the system is taking

Several signals can tell us which path the system has taken.

first, whether Oil prices remain elevated or begin to fall.

second, whether Inflation expectations continue to rise.

third, whether Bond yields remain under pressure or begin to stabilize.

Fourth, whether policymakers begin to emphasize financial stability rather than fighting Inflation.

Fifth, whether corporate refinancing becomes difficult and dominates discussion in Markets.

If Oil falls, the chain begins to unwind.

If yields remain high, funding remains under pressure.

If refinancing becomes the central issue, the problem has moved from Markets to Companies.

What causes the reflexivity loop to stop

Reflexive systems do not run indefinitely. At some point something interrupts the chain.

In the current environment several things can do that.

1. Oil prices stabilize

If energy stoppages cease, Inflation expectations will cool. When Inflation expectations fall, Bond yields will stabilize. And when yields stabilize, the chain begins to unwind.

2. Policymakers change priorities

If central banks and governments focus from fighting Inflation to protecting financial stability, funding conditions will ease. Liquidity will return. The loop will lose power.

3. Markets adapt

Sometimes the system adapts. Companies hedge energy exposure, supply chains reroute, inventories normalize and the same headlines will no longer produce the same Fear response.

The loop does not end when Fear goes away. It ends when Fear stops creating the same scale of behavior in the system.

Conclusion

Reflexivity is not merely a theory regarding bubbles. Reflexivity is a framework for understanding how pressures move through the system.

A geopolitical event becomes an energy event.

An energy event becomes an Inflation event.

An Inflation event becomes a rate event.

A rate event becomes a funding event.

A funding event becomes a corporate event.

Markets are not simply observing events. Markets are amplifying those events. And sometimes helping determine what those events become.

In reflexive systems, price does not only describe reality. Price helps create it.

Markets do not travel in straight lines. Markets travel in loops. And the most important loops are often invisible until they have already shaped the system.

A geopolitical event becomes energy Stress.

Energy Stress becomes Inflation pressure.

Inflation pressure becomes funding pressure.

Funding pressure becomes reality for corporations.

That is reflexivity.