The Freight Recession Is Starting to Price the Survivors

What recent trucking deals say about asset values, book value, and Universal Logistics.

The easy trucking story starts with diesel. Diesel goes up, fuel surcharges follow, customers absorb part of the cost, and carriers protect their margins. Simple story. Too simple.

Diesel does not make a weak trucking company strong. It exposes the carrier that bought equipment at the wrong time, financed it at the wrong rate, ran too much spot freight, underpriced insurance, and assumed the pandemic freight market was normal. A stronger carrier has contract freight, fuel tables, procurement scale, routing discipline, customer relationships, claims data, maintenance systems, and enough balance sheet to wait. A weaker carrier has a truck, a payment, an insurance bill, and a fuel card.

That split is where the story starts.

This is not really a diesel article. It is about what happens when diesel, weak rates, higher insurance, maintenance inflation, expensive debt, and excess capacity grind the same industry for several years. At some point, the cycle stops being only an earnings problem and becomes an ownership problem. The small carrier parks trucks. The owner-operator leaves the market. The private fleet sells. The weak broker loses volume. The tired seller takes a call. The strong buyer starts doing math.

The article is not a buy list. The payoff is narrower: if private buyers are still paying real money for freight assets after several years of pain, then the public market may still be valuing some companies off the wrong year.

That is where Universal Logistics enters.

Messy, leveraged, uncomfortable, and still asset-heavy enough to deserve real work.

The cycle is repairing, not booming

This does not look like the beginning of a freight boom. It looks more like the late stage of an oversupply cycle.

A boom is easy to spot. Volumes accelerate, rates rise, earnings turn, and everybody sees the same thing. This is not that. Demand is still uneven. The consumer is not suddenly heroic. Industrial freight is not roaring everywhere. The economy is not handing carriers a perfect tailwind.

The change is on the supply side.

The pandemic freight boom pulled too much capacity into the market. Too many trucks, too many small fleets, too many people financing equipment against rates that were never normal. Then the cycle turned. Rates fell. Fuel stayed painful. Insurance stayed ugly. Maintenance got more expensive. Debt costs moved higher. Used equipment stopped bailing everyone out.

The weak carriers did not all die in one headline. They just kept losing air. A carrier exits one lane. Another sells trucks. A private owner decides the next insurance renewal is not worth it. A driver moves to a stronger fleet. A customer shifts freight to a carrier that still answers the phone.

This is how the cycle repairs itself: not through a beautiful demand recovery, but through exhaustion.

By the time earnings look better, part of the asset transfer has already happened. Recent deals matter because the assets are being marked after the pain, not before it.

Fuel gets the headline because everyone sees the price. Insurance may be just as important. A large carrier can spread claims, invest in safety systems, bring data to renewal discussions, and absorb a bad year without disappearing. A small fleet often takes the renewal as it comes. When rates are weak, insurance is not just an expense line. It is a survival test.

Government help is not the thesis either. Canada has had temporary fuel-tax relief, which helps at the margin but does not turn a poorly financed fleet into a high-return business. In the United States, the relevant programs are mostly tied to emissions, cleaner fleets, diesel reduction, energy efficiency, and equipment transition. Useful for certain fleets. Not a broad diesel bailout for public trucking companies.

The real relief is structural. Weak capacity leaves. Stronger operators get more oxygen. Buyers with balance sheets pick through the assets. Government can soften a few edges. The cycle does the cutting.

The private-market tape

The public market sees damaged earnings. Strategic buyers see yards, trucks, trailers, contracts, drivers, customer lists, freight density, terminals, and routes that may be worth more inside a stronger system. A stock screen sees weak current earnings and says no. A strategic buyer asks what the same assets could earn under better discipline.

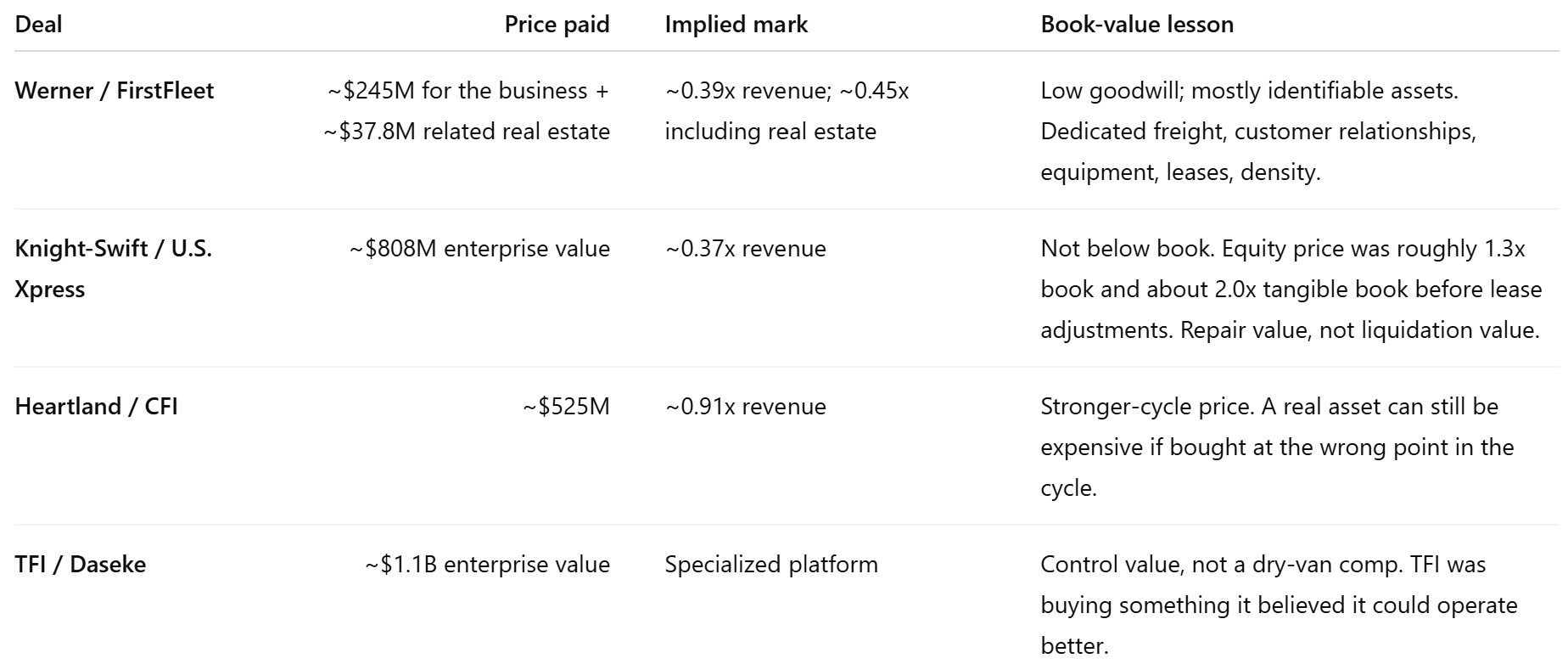

The recent tape is not perfect, but it is useful.

The table does not give one magic multiple. It gives a map.

A damaged truckload network can look cheap on revenue but not cheap on tangible book. A dedicated carrier can be bought at a modest revenue multiple with most of the price tied to identifiable assets. A stronger-cycle platform can command a much higher sales multiple. A specialized freight platform has to be valued around control and execution, not generic trucking exposure.

There is no single answer to “what is trucking worth?” There is asset quality, timing, leverage, customer mix, buyer discipline, and what the buyer can fix. The point is not to prove that every trucker is cheap. The point is to see what real buyers paid when earnings were broken.

The tape is useful, but it is not perfectly clean. U.S. Xpress gives the best public book-value comparison because it was a public company. FirstFleet gives something different: purchase accounting, low goodwill, and identifiable assets, but not a standalone public book value. CFI gives a stronger-cycle transaction mark, mostly through revenue and adjusted earnings, but not a clean book-value test. Daseke gives control value in specialized freight, not a simple dry-van comp.

So the table should not be treated as one perfect multiple. It is a valuation map. What kind of trucking asset, at what point in the cycle, under what buyer — those details decide the price.

Below

The setup is above. Now comes the part I care about most: the prices. What Werner actually bought, why U.S. Xpress was not cheap on book value, what CFI and Daseke say about timing and control, and why Universal Logistics is the first messy public name where the asset math is worth doing.