What Would Greg Abel Do?

The quiet Canadian who inherited Warren Buffett’s empire — and the code that keeps it alive.

🚨 Join 100+ readers before tomorrow’s cockpit unlock.

The full Weekend Plus drops Sunday — scenario map, credit curves, and the 10-day flight path.

Don’t watch from the gate — board early →

I. The Heir in Silence

Omaha wakes differently now.

The letters are shorter. The crowd is smaller. The Oracle is gone.

But in the quiet hum of the Berkshire headquarters, one light still flickers before dawn.

Greg Abel — the man most people outside Wall Street couldn’t pick out of a lineup — reviews cash-flow statements with the calm of a surgeon. No quotes, no jokes, no theatrics. Just the same discipline that turned a regional utility into one of America’s most profitable infrastructure empires.

He’s not Buffett’s spiritual twin. He’s his operational antithesis — and that’s exactly why he’s here.

Buffett loved to buy pieces of great companies.

Abel built entire ones.

He was never a storyteller. Never needed the spotlight. His only visible emotion is precision. If Buffett was the philosopher-capitalist, Abel is the engineer-steward — a builder who doesn’t confuse charisma with competence.

Between the lines: “When the music stops, the quiet ones are still working.”

II. The Operator’s DNA

Abel’s story begins far from the marble floors of Omaha — in Edmonton, Alberta.

A prairie kid who learned early that cash is colder when you have to earn it.

He joined PricewaterhouseCoopers out of college, then migrated to energy trading, eventually finding his home at MidAmerican Energy — the company Buffett later folded into Berkshire Hathaway Energy.

In two decades, Abel transformed it from a patchwork of regulated utilities into a fortress of predictable returns.

He mastered the three currencies Buffett prized most: cash, time, and trust.

He avoided the glamour of tech, the frenzy of Wall Street, the moral hazard of leverage.

He built duration.

When Buffett saw that, he didn’t just see a manager — he saw a system: a man who could run 90 % of Berkshire’s industrial empire with zero drama.

Abel’s fingerprints are on every steady machine under the Berkshire umbrella — pipelines, railroads, real estate, renewables.

He’s the reason Berkshire Energy’s assets climbed from $22 billion in 2000 to over $140 billion today, with virtually no dilution and no showmanship.

He doesn’t pontificate about market cycles; he lives through them.

Between the lines: “Buffett bet on character. Abel industrialized it.”

III. The Berkshire Dilemma

Now comes the paradox.

Berkshire Hathaway, the most admired conglomerate in financial history, has become too large to outperform.

Its market value flirts with $900 billion. Its cash pile hovers near $180 billion. The math of compounding has become the math of gravity.

In 1970, a small arbitrage could move the needle. In 2025, even a $10 billion acquisition barely registers.

Greg Abel inherits not just a portfolio — he inherits the constraints of perfection.

He must answer the question no CEO of Berkshire has ever faced:

How do you compound rationality when the world is already priced for it?

Berkshire’s investors still expect Buffett’s touch — opportunistic buys, letters of grace, patience rewarded by timing.

But the market has changed. It’s faster, more indexed, less forgiving.

If Buffett’s genius was to buy when others panicked, Abel’s test will be to act when no one panics — to make money in an era of ambient complacency.

He’s walking into a world that rewards noise, while he was built for silence.

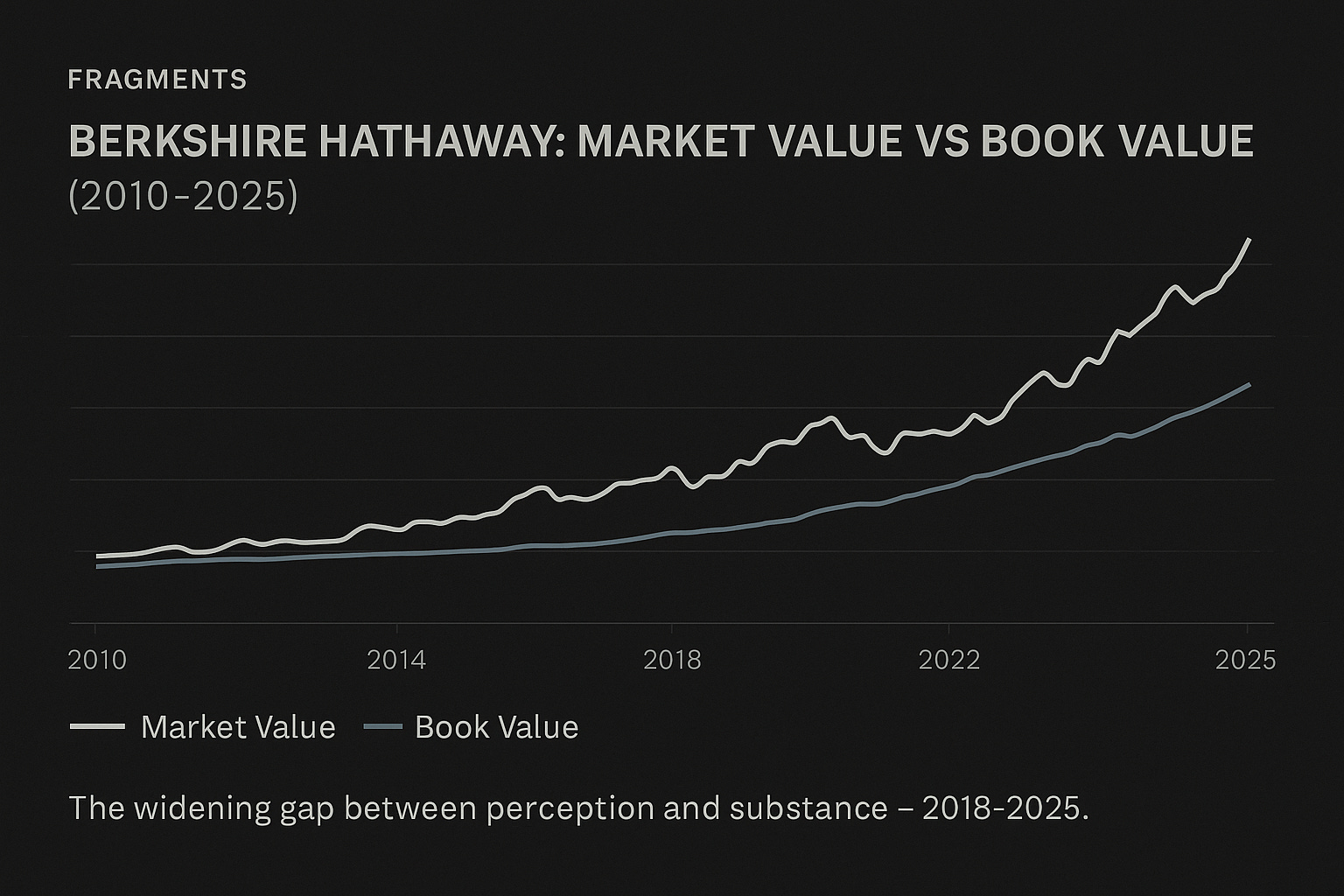

Chart — Berkshire Hathaway: Market Value vs Book Value (2010–2025)

A gentle slope becomes a plateau. Market cap up 4×, book value only 2×.

The gap between perception and substance — widening quietly since 2018.

Between the lines: “Even fortresses collect dust when the tide doesn’t move.”

⚙️ (Below the fold: the flashback from Buffett’s final year, the Capital Code, three scenarios, and the flight plan for Berkshire’s next decade.)